This Freight newsletter covers a summary of current industry topics, market trends, freight service provider financial results, and a view to the future for major freight industry segments.

Current Industry Topics

FedEx Freight Spin-Off as a Stand-Alone Company

In 2024, FedEx announced its plan to spin off its FedEx Freight LTL business as a separate company. The time is near as the official start date of June 1st is approaching. The size of this transaction makes it the industry’s largest over multiple decades.

Revenues for the new FedEx Freight are estimated at $9.0 billion, making it the largest stand-alone LTL provider in North America – over 50% larger than #2 Old Dominion Freight queue. A couple of notable items:

- Contracts – For years, FedEx offered bundled discounts across Small Parcel and LTL Freight to entice shippers to utilise FedEx for all of those needs – bundling programs are being discontinued.

- Focus – The spun-off FedEx Freight has indicated that it will shift away from “chasing volume” to focus on high-yield, high-margin freight. As the new FedEx Freight realigns its customer base, market share opportunities should arise for those carriers interested in lower-yield, lower-margin customers. At the same time, those carriers currently focused on high-yield, high-margin freight will see significant new competition.

Where are my Trucks? Why are my freight costs rising?

Industry change is upon us, and it may not be temporary. Capacity is leaving the market, and costs are rising. Perhaps RXO Chairman/CEO Drew Wilkerson said it best: “The capacity reductions in the industry represent one of the largest structural changes to truckload supply since deregulation and should set the market up for a sharper inflection when demand recovers.”

- Fewer Drivers – we have commented previously about the crackdown on Non-Domiciled Commercial Driver’s Licenses (CDL’s) that, over the short term, will remove up to 200,000 drivers from the market as non-residents fail to meet requirements, including English proficiency.

- Carrier Exits / Consolidation – with rising costs, small companies and individual owner operators are electing to exit the business as their operations are no longer profitable.

- Fewer ELDT’s – Entry Level Driver Training (ELDT) schools have come under recent well-deserved scrutiny by the Federal Motor Carrier Safety Administration, removing upwards of 7,000 ELDT’s from the Training Provider Registry for sub-standard operations over the last 5-6 months. Inadequate training has been linked to several high-profile accidents involving commercial motor vehicles, primarily trucks. While intended to improve safety for the long-term, short-term training capacity could drop by 20% plus.

Summary: Significant changes in the landscape of freight service providers, along with decreasing capacity, certainly in the near term, are strong reasons for shippers to solidify relationships with their important freight service providers now.

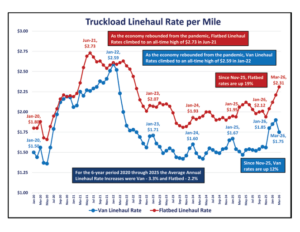

The Market - Truckload Rates, Diesel Fuel Prices

Two barometers of the Freight market over time are Truckload Linehaul Rates per Mile and Diesel Fuel Price per Gallon. The charts shown here were developed using data from the Department of Energy and from DAT Freight and Analytics.

Coming down from post-pandemic peaks, Truckload Linehaul Rates per Mile stabilised from Jan ‘23 through Nov ’25. However, over the last 4 months

- Van Linehaul Rates per Mile are up 12% to $1.75

- Flatbed Linehaul Rates per Mile are up 19% to $2.31. Reduced capacity is causing market rates to increase.

Coming down from the steep rise in average monthly Diesel Fuel Prices due to Russia’s invasion of Ukraine, the monthly Average Diesel Fuel Price per Gallon stabilised from Jan ‘24 through Feb ‘26, ranging between $3.49 and $4.04.

Because of the military campaign against Iran that began on February 28th, Diesel Fuel Prices have spiked 32% to $4.92 in March. Current weekly Diesel Fuel Prices per gallon are well over $5.00.

Summary: Linehaul Rates and Diesel Fuel Prices are volatile and often move dramatically with extraordinary events as shown in the charts above. Shippers need to be ready to react quickly to marketplace changes.

What the Numbers Say

One way to assess the state of the freight industry is to review recent financial results from key players. The tables below summarise North American Financial Results for 15 large industry players combined, comparing Full Year 2025 vs 2024 and Q4 2025 vs. Q4 2024.

The Full Year table above illustrates that 2025 was difficult for Freight Service Providers, as Revenues, Profits (EBITDA), and Margins are down year over year. A bit of a silver lining appeared in Q4 2025, as Revenue and EBITDA versus Q4 2024 showed improvement from Full Year 25 comparisons to Full Year 24.

A deeper dive for 2025 into four of the largest and most recognisable Freight Service Providers is summarised in the table below.

A few observations –

- At (5.5%) year over year, Revenues for these top 4 providers were down nearly double the overall average of (3.1%) - J.B Hunt was nearly flat due to the strength of their intermodal business

- EBITDA was down 9.8%, mitigated by the +30.5% improvement at C.H. Robinson due to stringent cost-cutting measures

- At a 31.9% margin, Old Dominion was by far the most profitable provider at more than two times the overall average margin of 12.5%

Summary: While the financial results above clearly demonstrate that the market continues to favour shippers over freight service providers, the balance has begun to shift away from a ‘shipper’s market’.

The Road Ahead

For the remainder of 2026 (Q2 – Q4), the market is transitioning from prolonged oversupply toward gradual rebalancing. Capacity remains generally available, but the most extreme shipper leverage phase is moderating — particularly in Truckload. Below, we captured key takeaways from multiple freight industry forecasts for 2026, organised by service type.

Truckload

- Demand is stabilising compared to 2025 lows as retail inventories are largely normalised, and manufacturing is showing modest improvement in demand. Seasonality volatility is becoming more pronounced due to a leaner carrier base.

- Supply is getting closer to balance as meaningful capacity attrition occurred in 2024-2025. This was driven by bankruptcies and small fleet exits. Driver availability continues to be structurally constrained due to enhanced regulations (Non-Domiciled CDLs).

- As supply gets closer to a rebalance with demand, rates will likely show upward movement (low-to-mid single-digit increases) in the latter half of 2026.

LTL

- Demand has improved modestly at the beginning of 2026, driven by E-commerce and retail restocking.

- Excess supply is shrinking as network discipline remains strong among major carriers. There has been limited terminal expansion and continued long-term driver constraints. The shortfall in LTL drivers is projected to reach as high as 160,000 by 2030.

- Rates will hold firm as General Rate Increases (GRIs) are sticking more consistently in 2026.

Intermodal

- Demand is stabilising after 2025 softness and import volumes improved in key ports.

- Rail service levels improved in major corridors. Equipment supply is adequate to meet the reduced demand with no major shortages anticipated in high-volume corridors.

- Excess supply will continue to hold rates flat with no likely increases at least through mid-2026.

Cross-Mode Themes

- Market rebalancing is underway. The freight recession is largely over.

- Carrier's financial health is improving.

- Negotiation leverage is narrowing.

Summary: What does this mean for shippers? With capacity continuing to shrink versus demand, now is the time to lock down Freight Service Providers with contracted rates to ensure service availability and consistent costs. In the current environment, by relying on spot-quotes instead of contracted rates, shippers run the risk of gaps in service along with spikes in freight costs.

---

About the Authors

With a combined 40+ years of direct industry experience, Forrest, Tim, and Robb have successfully delivered well over 100 projects to their clients with annual savings in excess of $25 million.

Forrest James

- Former Major, United States Air Force - graduate of the United States Air Force Academy

- Former COO / CFO and head of consulting for BestTransport, Inc

- 20 years with ERA Group as a Freight consultant

Tim Malarkey

• Former Corporate Vice President, American Greeting Corporation

• Former practicing CPA with PricewaterhouseCoopers (PWC)

• 17 years with ERA Group, partnering with Forrest James

Robb Lusk

• Former Director of Supply Chain, Del Monte Foods

• Led various cost optimisation projects with Del Monte, totaling $12M in annual savings

• Has saved ERA Group clients $5M to date

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)