ERA Group's quarterly insights regarding market conditions, potential impacts on procurement, and supply chain planning.

Geopolitics, Tariffs, and Supply Chain Costs

Global supply chains entered Q2 2026 under continued pressure from geopolitical instability, new tariffs, and transportation volatility. Conflict in the Middle East and the recent U.S. blockade of Iran at the Strait of Hormuz has disrupted shipping routes, increased war-risk and fuel surcharges, and raised insurance costs while creating booking uncertainty across key trade lanes. For example, Brenntag’s March 9 shipping update noted rerouting around the Cape of Good Hope, temporary fuel surcharges on multiple lanes, war-risk charges of roughly $2,000-$4,000 per container, and growing marine-insurance constraints in the Gulf.1

Recent diplomatic headlines have caused sharp day-to-day swings in oil prices, and the broader energy and freight environment remains highly unstable. Reuters reported on April 13 that oil surged again after the U.S. expanded pressure on Iran and concerns over supply flows through the Strait of Hormuz intensified, even though prices later pulled back on hopes of renewed talks. Carriers also remain cautious: Reuters reported that Hapag-Lloyd said the situation is still difficult to assess and that insurance and navigation conditions remain challenging.2,3

At the same time, tariff policy continues to raise baseline import costs. A temporary 10% Section 122 tariff is now in effect on most imported goods into the United States through July 2026, adding incremental cost to imported materials across many industries.1

KEY TAKEAWAYS: Even when commodity markets settle temporarily, freight and tariff costs can still keep landed costs elevated. Buyers should treat logistics as an active part of sourcing strategy right now: shorten buying cycles where possible, ask suppliers to show exactly how surcharges are triggered, and avoid committing too far forward when freight conditions can change quickly.

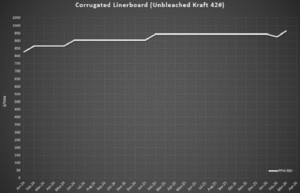

Corrugated

Containerboard pricing shifted direction quickly in early 2026. Industry data showed a price decrease in February, reflecting softer demand and competitive market conditions.4 Shortly afterward, producers announced new price increases in March, as operating costs remained elevated and mills continued to manage capacity levels carefully.5

In practice, some suppliers are not passing through the full February decrease before implementing the new increase. Instead, they are applying smaller net increases or delaying adjustments, effectively smoothing pricing over time rather than allowing a short-term decrease followed by a larger increase. This reflects continued cost pressure and a desire to stabilise margins, while demand remains moderate. 4

Immediately following the March increase, RISI announced another $30/tonne increase (net $50/tonne increase YTD) on April 17, 2026, as producers work toward full recognition of previously announced price hikes. Some forecasts suggest companies could pursue additional increases later in the year, if seasonal demand strengthens.4 Supply remains stable, and availability is generally good across most grades, but pricing direction is expected to trend gradually upward rather than sharply.

Chart Data: Pulp and Paper Weekly RSI Index[/caption]

KEY TAKEAWAYS: Corrugated pricing is still being managed more by supplier behaviour than by a clean pass-through of index moves. That means buyers should look beyond the published index and make sure suppliers are applying decreases and increases consistently. Short benchmarking exercises, competitive quotes, and clear pass-through maths will matter more than waiting for the market to correct itself.

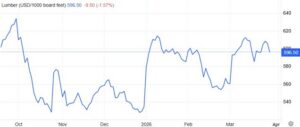

Lumber & Pallets

Pallet and pallet-grade lumber markets remain generally stable entering Q2 2026, but cost pressure is beginning to build. Hardwood supply is adequate in most regions, though tight availability of pallet lumber inputs is creating mild upward pressure on pricing, as seasonal demand starts to increase.6

Lumber prices have shown modest strengthening in recent weeks, and some sawmills have issued price increase notices tied to higher fuel, labour, and transportation costs. 5 However, housing demand has softened recently, with U.S. housing starts declining and builder inventories increasing, which has forced some price reductions in the construction market and helped limit sharper lumber price increases.7

Chart Data: TradingEconomics.com[/caption]

Supply remains available, and availability is generally good across most pallet grades. As spring shipping activity increases and input costs

continue to rise, buyers should expect gradual upward pricing pressure through Q2, but not broad shortages or sudden price spikes.

For the last four weeks, there has been a steady stream of increased requests, whether it’s driven by lumber pricing or excessive fuel surcharges. Some regions are experiencing more price pressure than others. The West is particularly expensive because it relies on commodities, while the green lumber in the East is still moving upward more slowly.

KEY TAKEAWAYS: This still looks like a slow regional tightening market, not a major supply shock. Buyers will usually get the best results from operational discipline — stronger pallet recovery, repair programs, and backup regional sources — rather than chasing spot buys after prices start moving.

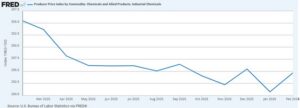

Chemicals & Gasses

Chemical markets entered Q2 2026 under cost pressure from volatile oil and energy markets, freight surcharges, and global supply disruptions tied to the Middle East conflict. Oil prices have swung sharply in recent days as markets react to developments around the Strait of Hormuz, and suppliers across multiple chemical categories are continuing to push through price increases and surcharges to offset higher operating and transportation costs.2,8

Several distributors have already announced new freight surcharges, including temporary invoice surcharges on shipments and rate increases of approximately $0.03 per pound on bulk and packaged chemical orders across North America.9 These surcharges reflect elevated transportation costs and ongoing supply chain volatility across the chemical sector.

[caption id="attachment_13704" align="aligncenter" width="589"]

Chart Data: Producer Price Index by Commodity: Chemicals and Allied Products: Industrial Chemicals[/caption]

As of April 13, 2026, below is a summary of the current chemical supply-chain landscape:

- The markets for petroleum-based chemicals are incredibly volatile…increases have ranged from 20-60% just since late March.

- An arbitrage situation has been created with European customers willing to pay considerably higher prices (300-400%) compared to what U.S.-based customers have been accustomed to paying recently.

- Some of the largest chemicals producers in the world have experienced disappointing earnings over the past year+, and they are looking for ways to make up for lost revenue in the global economy.

- More chemicals price increases are likely to come, and we may end up with a force-majeure/allocation situation, depending on how things continue to develop in the Strait of Hormuz.

- Customers should also expect to pay more for sulfur-based chemicals, as there is a current global sulfur shortage.

Looking ahead, chemical pricing is expected to remain volatile through Q2 as oil markets, shipping lanes, and insurance conditions continue to react to Middle East developments. While availability remains generally adequate currently across most commodity chemicals, buyers should anticipate continued price increase announcements, freight surcharges, and selective supply constraints in energy-intensive products.3,8

KEY TAKEAWAYS: Chemical buyers should keep an eye on oil, energy, and freight together. Even if oil pulls back from a spike, pricing may stay elevated if suppliers continue to layer in freight surcharges and temporary adders. The best approach is to push for time-limited surcharges, clear reset points, and index-based formulas so costs can move back down if conditions improve.

Plastics

Plastic resin pricing remains unstable entering Q2 2026. Crude oil has been highly volatile, and recent pullbacks have not eliminated risk. Polyethylene and polypropylene markets are still facing higher costs tied to Middle East disruption, freight pressure, and supply chain uncertainty. 1,3 4

Reuters reported in late March that Middle East disruption had pushed polyethylene and polypropylene prices higher, as petrochemical flows through the Strait of Hormuz were disrupted.12 Ferguson’s March 30 market update likewise showed that resin markets were moving higher and that suppliers were responding to rising costs and tighter global conditions.13

[caption id="attachment_13705" align="aligncenter" width="541"]

Chart Data: TradingEconomics.com[/caption]

Even when oil pulls back, shipping conditions have not fully normalised. Reuters reported on April 13 that tanker flows and supply expectations remain highly sensitive to developments around the Strait of Hormuz, while Hapag-Lloyd said the impact on shipping remains difficult to assess because of mines and insurance complications.2,3 As a result, buyers should expect suppliers to remain cautious on quote duration and spot availability until freight conditions improve.

KEY TAKEAWAY: Resin buyers should not assume that a softer oil market will immediately translate into lower resin pricing. With Middle East disruption still affecting freight, quote duration, and supplier caution, plastics pricing may remain firm even if crude pulls back. In the near term, shorter buying intervals, backup domestic options, and contract protections around freight and force majeure are the safest way to manage the uncertainty.

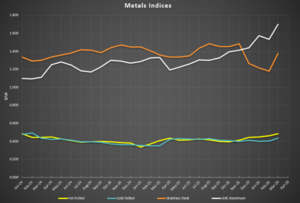

Metals

Steel pricing entered Q2 2026 on firm footing with mills continuing to manage production carefully and resist price concessions, while aluminium prices reached their highest levels since 2022. Domestic supply remains stable, and imports are still running below typical levels, helping keep pricing steady even as demand varies across industries.10 Recent pricing data shows a noticeable rebound in several steel categories from February to March, reinforcing the view that prices are stabilising and beginning to trend slightly higher heading into Q2.11

Tariffs are once again becoming an important factor in metals pricing. Recent policy adjustments affecting steel, aluminium, and copper signal continued government support for domestic producers, reinforcing a higher cost floor for these materials and reducing the likelihood of meaningful price decreases in the near term.12

[caption id="attachment_13706" align="aligncenter" width="531"]

Chart Data: BusinessAnalytiq[/caption]

KEY TAKEAWAY: Metals buyers are still facing a market where tariffs and mill discipline are keeping a floor under pricing. In that environment, expanding supply options and improving timing flexibility will usually create more leverage than pressing a single supplier harder on price. Where possible, use volume commitments to secure supply, but pair them with price protections or bands instead of fully fixed expectations.

----

About the authors

Travis Cantrell and Patrick Garr are Manufacturing Specialists at ERA Group. They both hold engineering degrees and have over 29 years of collective experience studying complicated client expenditures in direct material, industrial chemicals/gases, packaging supplies, and factory consumables/MRO. ERA utilises its in-depth subject-matter expertise to negotiate with suppliers and deliver best-in-class sourcing solutions for their clients.

_______

Sources:

1-Brenntag, Shipping and Tariff Updates, March 9, 2026.

2-Reuters, “Oil prices autumn as U.S.-Iran dialogue hopes ease supply concerns,” April 13, 2026.

3-Reuters, “Hapag-Lloyd says U.S. plans to block Hormuz difficult to assess,” April 13, 2026.

4 - Containerboard prices post surprising dip in February 2026, Packaging Dive, February 23, 2026

5 - Containerboard producers announce price increases for March 2026, Packaging Dive, March 28, 20266 - ePallet Monthly Pallet Market Update, March 2026

7 - Lumber Market Outlook, Trading Economics, April 2026

8 - Reuters, “IEA ready to further tap global oil reserves if needed, chief says,” April 13, 2026.

9 - Dow Industrial Solutions Freight Surcharge Notification, March 17, 2026

10 - Majestic Steel USA, CORE Report, March 27, 2026

11 - Business Analytiq Indices (hot rolled, cold rolled, galvanized sheet, stainless steel plate)

12 - Trump Administration Adjusts Steel, aluminium, and Copper Tariffs, Packaging Dive, April 4, 2026

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)